When it comes to AI, people who haven't caught the wave and are buying emerging stocks often dismissively say, "It's a bubble," or "It's over." But those kinds of crude assertions usually miss the mark. I used to be the one saying those things with a smug face, only to end up quietly shutting up later, so I understand the feeling all too well.

This time, instead of forcing it into past bubble patterns based on "vibes," I want to look at the investment status and free cash flow of hyperscalers.

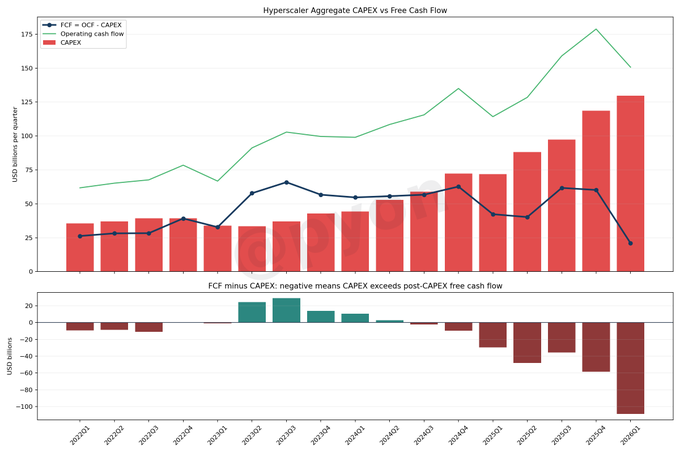

I looked at four companies: Microsoft, Amazon, Alphabet, and Meta.

CAPEX: Capital expenditures—money poured into the "boxes" that run AI, like data centers, servers, and GPUs.

FCF: Free Cash Flow The cash remaining after subtracting CAPEX from the cash earned through operations. It's the company's "stamina gauge."

In short, CAPEX is how much they've invested, and FCF is whether they are still breathing.

CAPEX is the money to build AI factories.

FCF is the cash left on hand after building those factories.

Right now, the factory construction rush continues, but the cash on hand is being significantly depleted.

Conclusion

So far, AI investment hasn't stopped, and the total CAPEX for the four companies is projected to increase to approximately $129.7 billion by Q1 2026. Meanwhile, FCF is shrinking to about $21 billion.

Simply put, while investment is increasing, the cash remaining after investment is thinning out, and they aren't making much profit yet.

The flow in the chart is quite straightforward: CAPEX is trending upward, FCF is stagnating, and the gap is widening.

The totals for Q1 2026 look like this:

- Operating Cash Flow: $150.7 billion

- CAPEX: $129.8 billion

- FCF: $21.0 billion

- Difference (FCF minus additional CAPEX): -$108.8 billion

The important point here is that FCF being positive is different from being able to comfortably absorb CAPEX. Since these are the mighty hyperscalers, they are acting composed for now, but their surplus is being heavily eroded.

The reason why it's a mistake to immediately judge this as "dangerous" and pivot to defensive or short positions is:

The AI market is ultimately an infrastructure investment like electricity; equipment comes before capital recovery.

Unspectacular things like data centers, power, semiconductors, and networks cost the most money. Therefore, what we should really watch is not just how "amazing" AI is, but how much cash they are burning. It's not over yet. The reason is simple: the revenue growth of major players is still strong, and cloud demand hasn't died out.

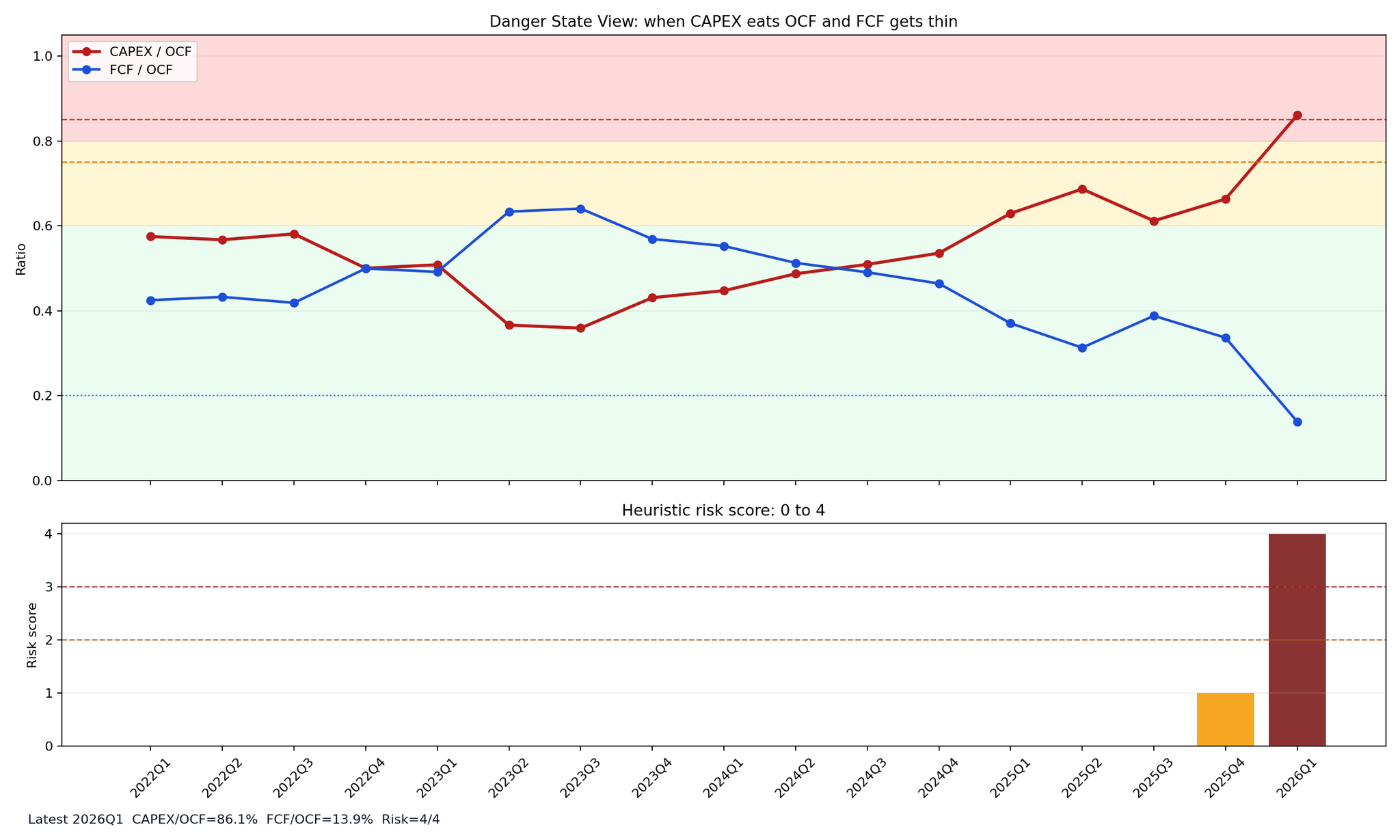

What's truly worrying isn't CAPEX itself, but the collapse of the assumptions that justified that CAPEX. Here are the points to watch:

- CAPEX / OCF stays high at over 90%

- FCF deteriorates significantly for two or more consecutive quarters

- Cloud growth rate falls below 20%

- Guidance is lowered

- Increased reliance on borrowing and leasing

One of these might be noise, but if 2 or 3 align, the situation is bad. As for when the first "moment of truth" will be, my estimate is around Q1 to Q2 of 2027.

Is CAPEX still increasing? Will FCF return? Or is investment just growing while monetization fails to keep up? If FCF doesn't return and only CAPEX piles up, then we can finally talk about this investment being truly dangerous.

For now, we are still in the middle of the process.

It's not that "AI investment is over."

It's a situation where "AI investment is still continuing (so as not to be left behind), but we're starting to wonder if it will really be profitable."

As a bonus, I created a risk score. Looking at Q1 2026, it's quite red. CAPEX exceeds 80% of OCF, and FCF is thin. Since it's infrastructure investment, heavy CAPEX is natural, but if FCF remains thin, the pressure for financing will rise. Even if sales are still growing, the atmosphere changes the moment people realize that what they thought was "buying the future" was actually a war of attrition.

Since I'm also on the side riding this bubble, I don't want to easily say the bubble will burst. But precisely because I'm on it, I can see that current AI investment is very heavy. The collapse will likely start from corporate growth rather than stock prices. For a while, the trend will be to keep dancing while keeping a close eye on the health of the hyperscalers.

This article is a personal analysis based on public information and financial data and is not intended as investment advice for specific stocks or assets. The content includes speculation and does not guarantee future performance, stock prices, or investment environments. Actual investment decisions should be made at the reader's own responsibility.