This is the most in depth report I have ever written, on a very exciting company.

If you read this article you will have a much deeper understanding of what Ouster does, how it plays into Physical AI, and what the future looks like.

Please Bookmark + Share this report.

There is NO paywall.

Enjoy!

I already briefly introduced Ouster in the Physical AI Layer 3 report.

Layer 3 is perception.

Perception is the part of the Physical AI stack where machines see, sense, and understand the world around them. A robot, drone, autonomous vehicle, factory system, or smart intersection has to know what is around it before it can make a useful decision. Ouster fit that layer because it gives machines a richer way to understand physical space through lidar, cameras, software, and smart infrastructure products.

But Ouster deserves a much deeper report now.

I believe that Ouster is trying to become a broader sensing and perception platform for Physical AI.

Let’s unpack that a bit.

Physical AI is the shift from AI inside screens to AI operating in the real world. The machine has to see the world, understand what is happening, decide what to do, act physically, then learn from the result. That loop is the foundation of the entire Physical AI theme.

Ouster sits near the front of that loop.

It helps machines sense the world.

It helps machines understand the world.

Then the robot, vehicle, drone, or infrastructure system can act on that understanding.

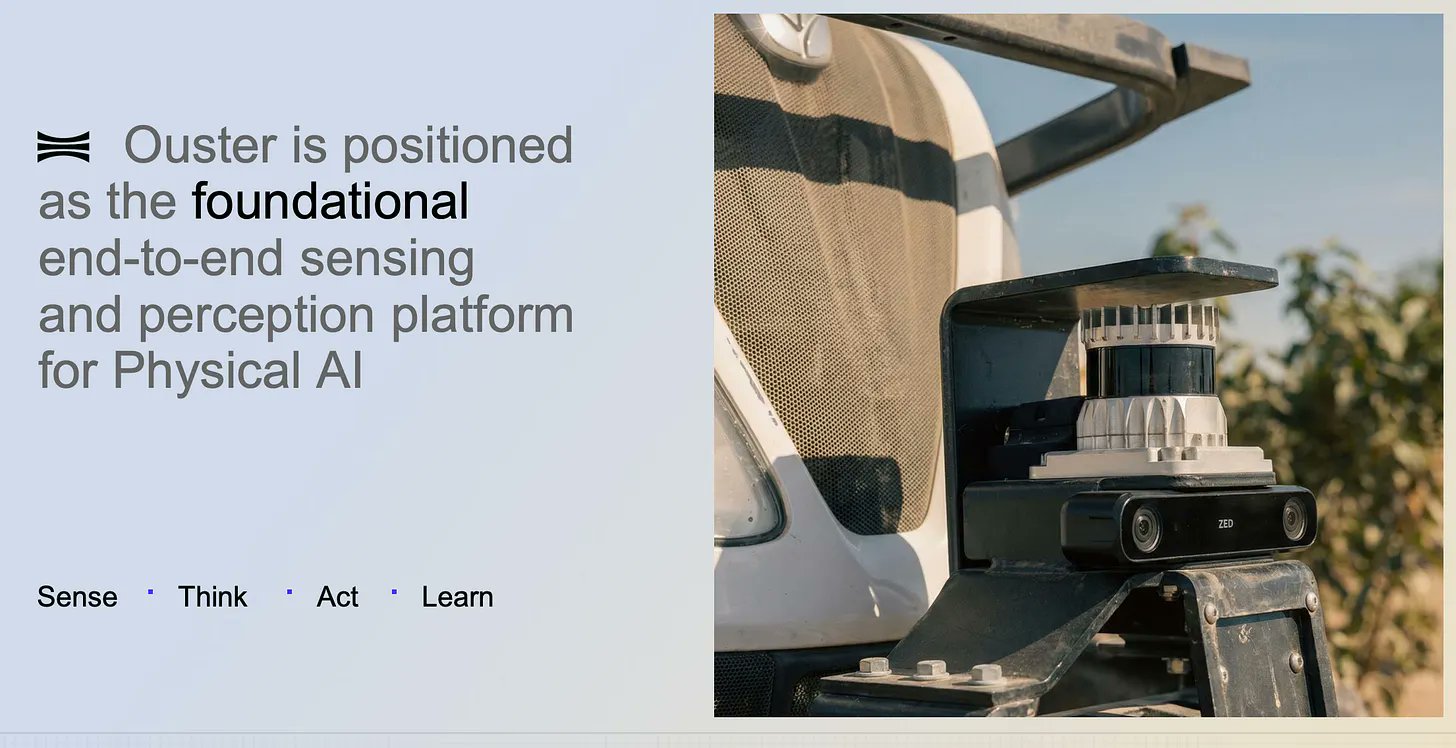

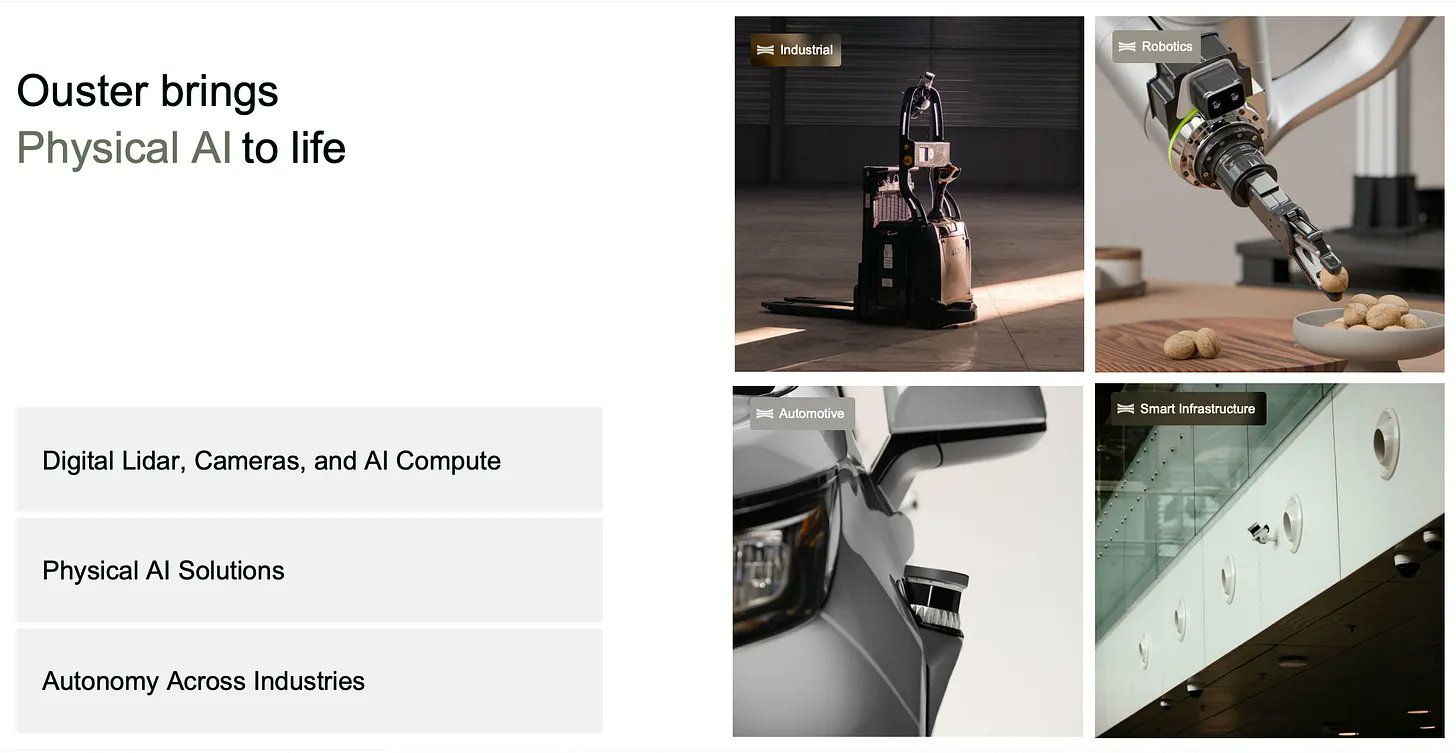

Their own Q1 2026 deck now frames them around Digital Lidar, Cameras, and AI Compute across Industrial, Robotics, Automotive, and Smart Infrastructure. It also says Ouster is positioned as the foundational end-to-end sensing and perception platform for Physical AI.

That is a big claim.

The purpose of this report is to figure out whether that claim is credible.

Why Does Ouster Belong Here?

The first question I want to answer is why Ouster is in my Physical AI basket.

While I am performing this research, I am looking for companies that touch the real-world machine loop.

- Sense

- See

- Understand

- Act

- Learn

This loop is what separates INTELLIGENT machines from your basic robot.

Ouster clearly sits in the sense, see, and understand portion of this loop.

It plays into this by selling the things that machines actually use to perceive their environment:

- Lidar

- Cameras

- AI compute

- Sensor Fusion

- Perception Software

And they sell it across many industries:

- Industrial

- Robotics

- Automotive

- Smart Infrastructure

They call themselves an ‘end-to-end sensing and perception platform for Physical AI’.

This is clearly one of the cleanest ways to own the perception layer. Directness. That is what I really want here. And Ouster sure is direct.

When I read through all the practical applications, I get:

- Warehouse robots needing toa void people

- Smart intersections needing to track vehicles and pedestrians

- Vehicles needing to build a 3d model

- Drones needing spacial awareness

- Machines in general just needing to know where objects are

- and so on

These are the problems that Ouster is trying to solve.

And unlike some of the other names in my basket, this isn’t future optionality.

It’s already happening today. They are making money.

But what’s great is that the whole Physical AI supercycle IS early.

I like that combination. Real revenue today. But still very early stages in the supercycle.

All the previously mentioned applications are really easy to understand how they are deployable today. But think about the future of robotics. We aren’t even in the first inning yet with robotics. Especially humanoids or humanoid like services.

And the last bit i’ll touch upon in this introduction is their breadth. I don’t quite remember when I first heard of Ouster, but I know I dismissed it. My lack of due diligence led me to thinking it was a Lidar company that was heavily tied to the automotive cycles that I really did not like investing in. And I heard so much talk about how Tesla will win without Lidar. I just really didn’t know any better.

So when I talk about breadth, I mean a few things.

First is all the industries that Ouster reaches in to.

But second is that they are much more than a Lidar story. We will get into that more as we go through this report, but really quickly they have:

- Stereo cameras

- Neural Depth

- Robotics vision

- AI compute adjacency

Physical AI systems will not use on universal sensor architectures. Different machines will use different stacks. And that’s where their breadth comes in.

This report is for educational and informational purposes only. It reflects my personal research process, opinions, and interpretation of publicly available information. It should be treated as general market commentary, not individualized investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, hold, short, or avoid any security.

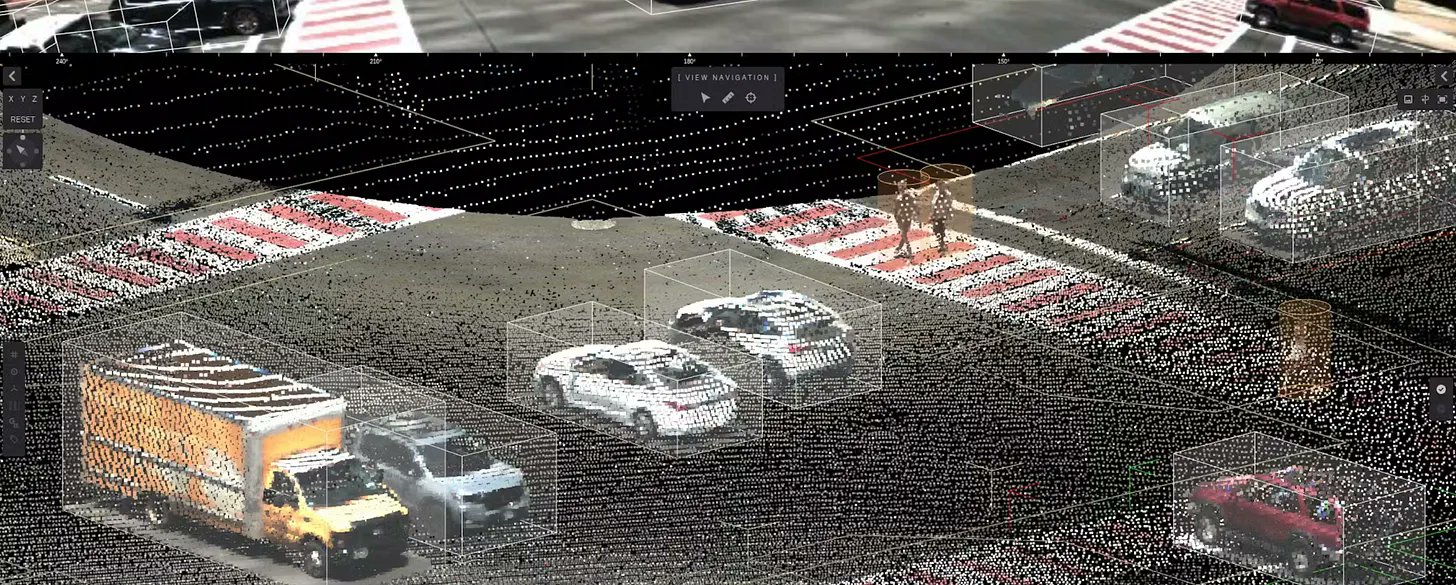

What Ouster Does

We will dive into more detail in all of these as we go through the report, but just to get you on track before hand.

1 - Lidar is the foundation. Ouster sells sensors that help machines measure the world in 3D.

2 - They also acquired Sterolabs which brought cameras into the story. This is great because cameras are important for visual context, robotics vision, and close-range manipulation. This is a meaningful expansion of what Ouster can offer.

3 - Then we have software. Gemini and BlueCity show that Ouster is trying to turn raw sensor data into actual customer outcomes. Rather than just getting a million data points in space, the customer wants actionable information like whether or not a person is in a restricted zone. This is the different between selling a sensor and selling perception.

4 - AI Compute helps process all of this data close to the machine. Lidar gives 3D structure, cameras give visual context, software interprets the data.

The Sensors: Lidar, Cameras, Stereo Cameras, and Radar

There are tradeoffs between the main ways machines perceive the world. A Physical AI system chooses sensors based on the job it has to perform.

Cameras, lidar, stereo cameras, and radar all see the world differently.

Let’s start with cameras because they are the easiest to understand. We know cameras. Right? They give visual detail. They can see color, labels, traffic lights, signs, cracks, people, packages, textures, and so on. This is great and useful because the physical world is designed for human vision.

But a normal camera sees a flat image. So the system has to estimate depth through software, movement, object size, perspective, or AI. That can work extremely well, but it is still estimating distance rather than directly measuring it.

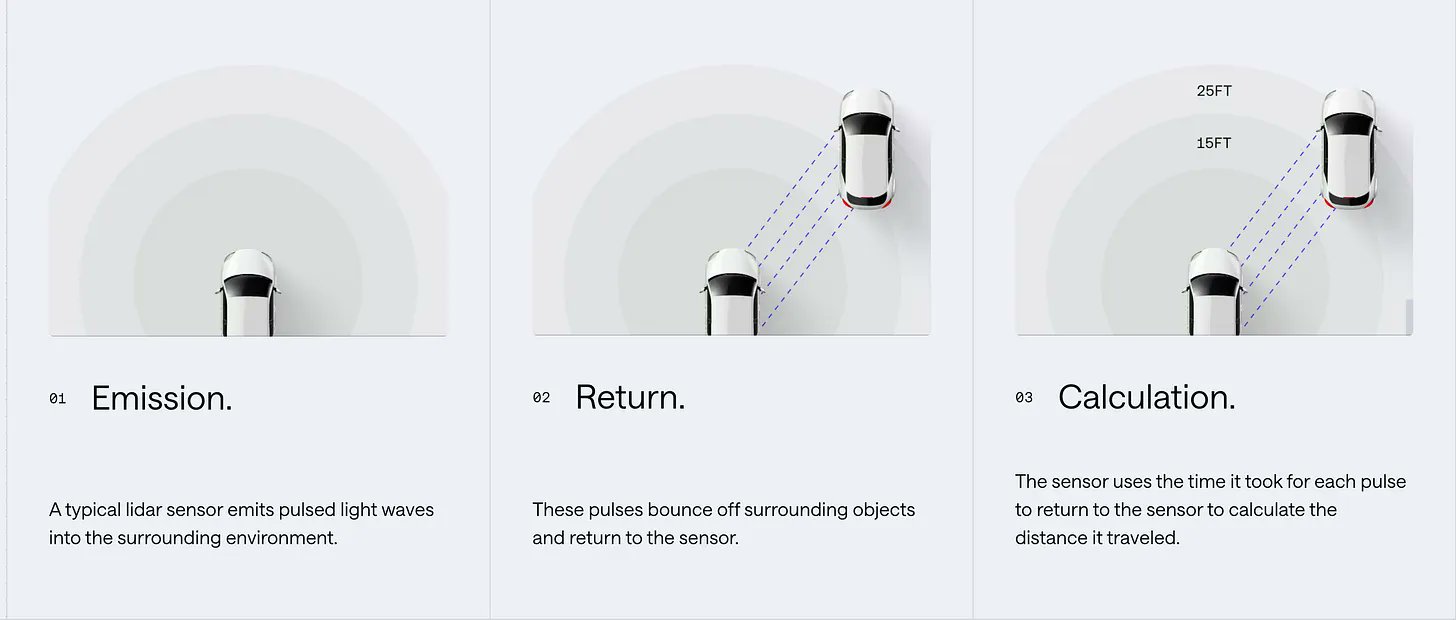

Lidar is different. Lidar sends out laser pulses and measures how long they take to return.

This gives the machine direct 3D distance. The special value here is geometry. Lidar helps the machine understand shape, distance, and location in physical space. That is why lidar can become especially valuable in mapping, smart intersections, industrial automation, ports, warehouses, mining, construction, and other environments where the machine needs to know exactly where things are.

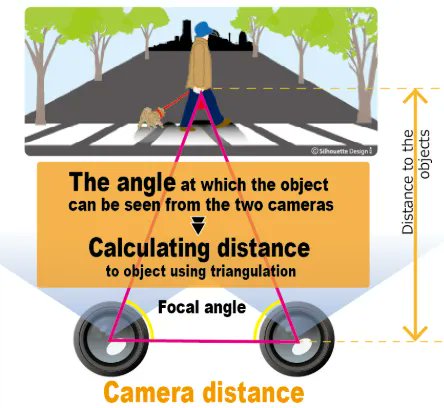

Stereo cameras kind of sit between these two ideas. They are still cameras, but they use two views to estimate depth. Similar to human eyes.

This is where the Stereolabs acquisition comes in. With this addition, Ouster now has exposure to camera-based depth too. This is important because some robotics applications, especially arms or humanoid hands, may care more about close-range visual depth than long-range lidar. A robot trying to grab an object may not need to see 500 meters away. It may need to understand the object right in front of its gripper. That is a different perception problem.

Then there is radar. Radar uses radio waves.

Its major strength is motion and speed. It can often work better in fog, dust, rain, snow, or poor visibility. The tradeoff is detail. Radar usually gives less object detail than lidar or cameras.

So to tie this together, Ouster’s current strategy makes much more sense once we understand that no single sensor solves every Physical AI problem.

They started with lidar, which gives direct 3D perception.

They added stereo cameras, which are useful for robotics vision, close-range depth, and manipulation.

Then Gemini and BlueCity add perception software, which helps turn the raw sensor data into something useful for the customer.

That is the key point. Physical AI systems will not use one universal sensor architecture. Different machines will use different stacks. A warehouse robot, smart intersection, drone, port automation system, humanoid hand, mapping vehicle, and mining machine all have different sensing needs.

So when you think about the Ouster thesis, you shouldn’t think “lidar wins everything.”

The better thesis is that machines need perception, and Ouster is trying to sell more of the perception stack.

If you are enjoying this article so far, please consider bookmarking & sharing! It's greatly appreciated.

The Tesla / Lidar Comments

I do want to address the common objection I hear whenever people talk about Ouster, regardless of whether this talking point is justified or not.

Tesla does not use lidar. So why should anyone care about a lidar company?

I understand the question. Tesla made the camera-first argument mainstream. The logic is that cameras are cheap, scalable, and supported by a huge vehicle data engine. Tesla controls the vehicle, software, compute, customer fleet, and update cycle. That gives it a unique advantage.

So yes, that argument deserves respect.

But I also think this is where a lot of people take the wrong shortcut.

Tesla is one company, one architecture, and one use case. It is focused on mass-market passenger vehicles.

Ouster’s opportunity is much broader than that. We are talking about all Physical AI applications I have mentioned up to this point. Those systems have different economics than a consumer passenger car.

A lidar sensor might be too expensive or unnecessary for one use case, but it can be a small cost relative to the value of safety, uptime, precision, automation, or mission performance in another.

So I think a better thing to focus on / explore is which physical systems need direct 3D measurement badly enough to pay for it?

That is the Ouster question.

I also wanted to include Ouster’s article and video about lidar versus cameras while driving in the rain. I won’t just restate the article, but I found it useful because it reinforces the idea that different sensors fail differently.

Lidar vs. camera: driving in the rain

https://www.youtube.com/watch?v=7QQKaurQW0Q

In the demo, Ouster argues that its lidar was less distorted than camera footage in moderate rain because of larger optical aperture, shorter exposure time, and digital return processing. But in the same breath, they also say wet roads can reduce lidar range on the road surface because water creates mirror-like reflections.

Lidar is not perfect. Cameras are not perfect. Radar is not perfect.

Each sensor has advantages and weaknesses. That is why sensor fusion can make the full system stronger.

Ouster does not need every passenger car to use lidar. It needs enough Physical AI systems across all the industries to decide that direct 3D sensing creates enough value to justify the cost.

So that is the setup. Ouster is not just one product anymore.

For this report, I’m going to break the business into three pieces: the core digital lidar business, the Stereolabs camera and robotics-vision business, and the Gemini / BlueCity software layer. The key question is how much of this is already showing up in revenue today, and how much is still platform optionality.

After that I will unpack their:

- End markets

- Manufacturing, Supply Chain, and IP

- Financials

- Unit economics + margins

- Path to profitability

- Competition

- Valuation + Financial Modeling

I am building out my entire Physical AI portfolio in real time. If you wan't to see which companies I am investing in, their entire deep dives, and the weightings for each, click here:

Core Digital Lidar

This was the original engine of Ouster.

And this is still the most proven part of the company today. In Q1 they shipped ~8,300 lidar sensors vs. ~4,300 camera sensors. So lidar is still the core hardware base even though they are broadening

Lidar gives machines a 3D measurement of thee world.

How far away is that wall? Where is the person? What is the shape of this road? etc.

Now the ‘digital’ part is the key Ouster-specific bit.

Older lidar systems were more analog and complex. Lots of separate parts, complicated optical alignment, more expensive hardware, and harder scaling.

Ouster’s argument is that it uses a more semidconductor-style architecture where they combine VSCELs (tiny lasers that send out the light), SPADs (very sensitive detectors), and custom SOCs (chips that process the signal and help turn them into distance data).

So again, the flow is:

- The sensor sends out laser light

- That light hits objects

- Some of the light bounces back

- The detector catches the returning photons

- The chip measures the timing

- The sensor calculates the distance

Do that over and over again very quickly, across many directions, and you get a point cloud.

This is a cloud of measured points in physical space. Each point says ‘something exists at this distance and angle’. When you have enough points, the machine can understand the shape of the scene.

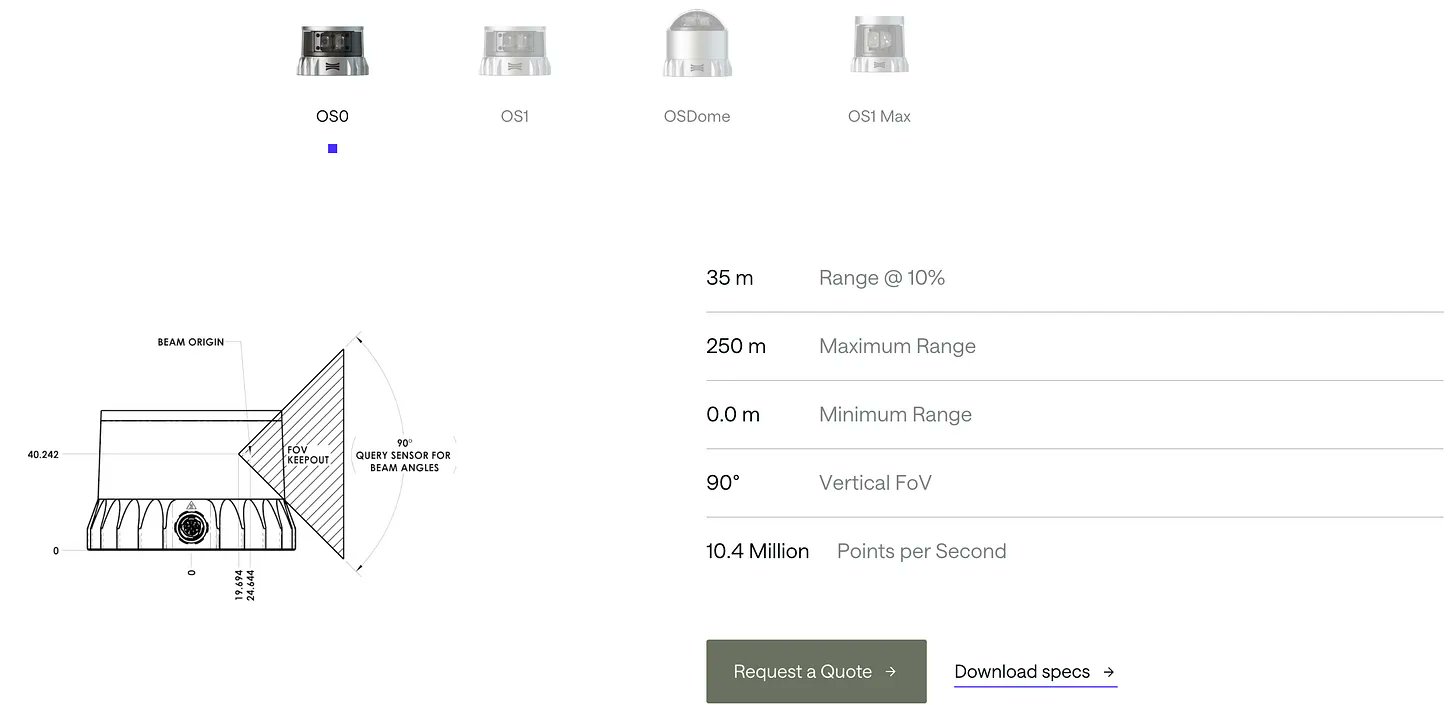

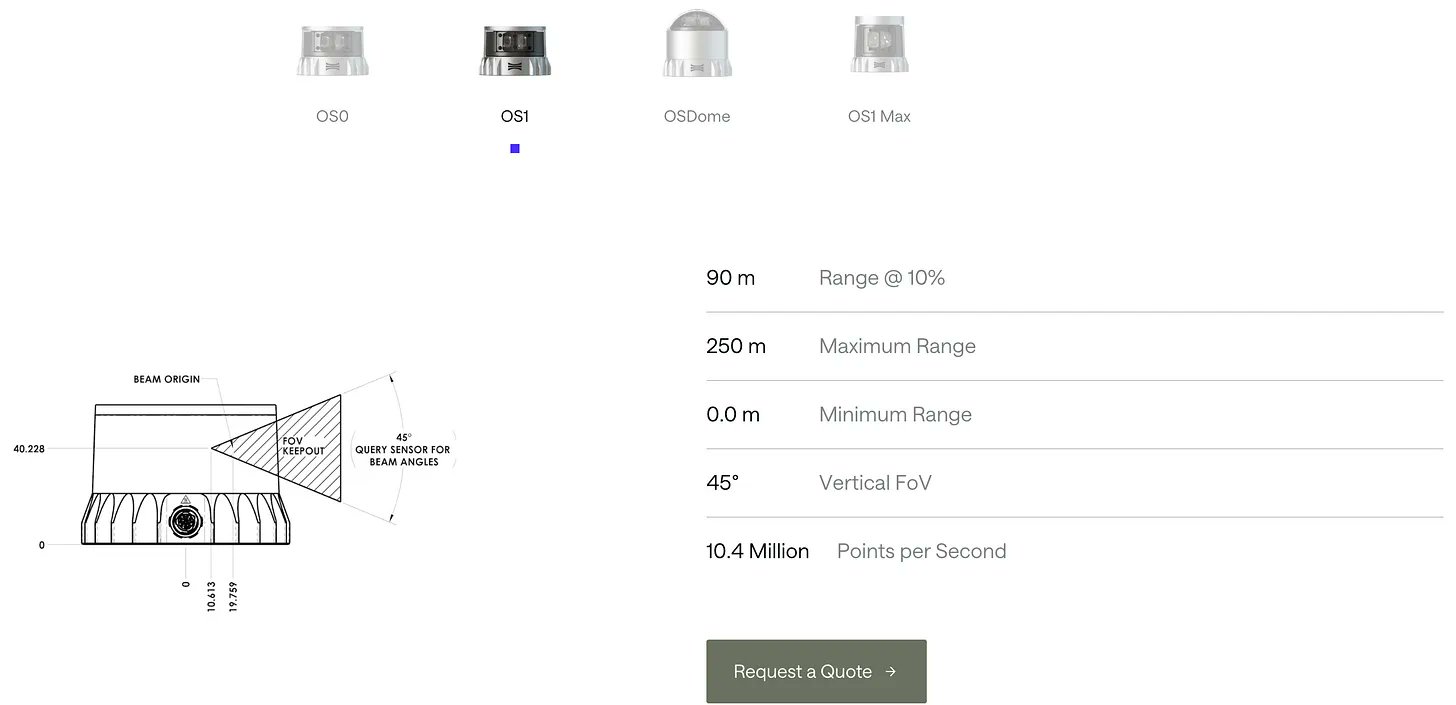

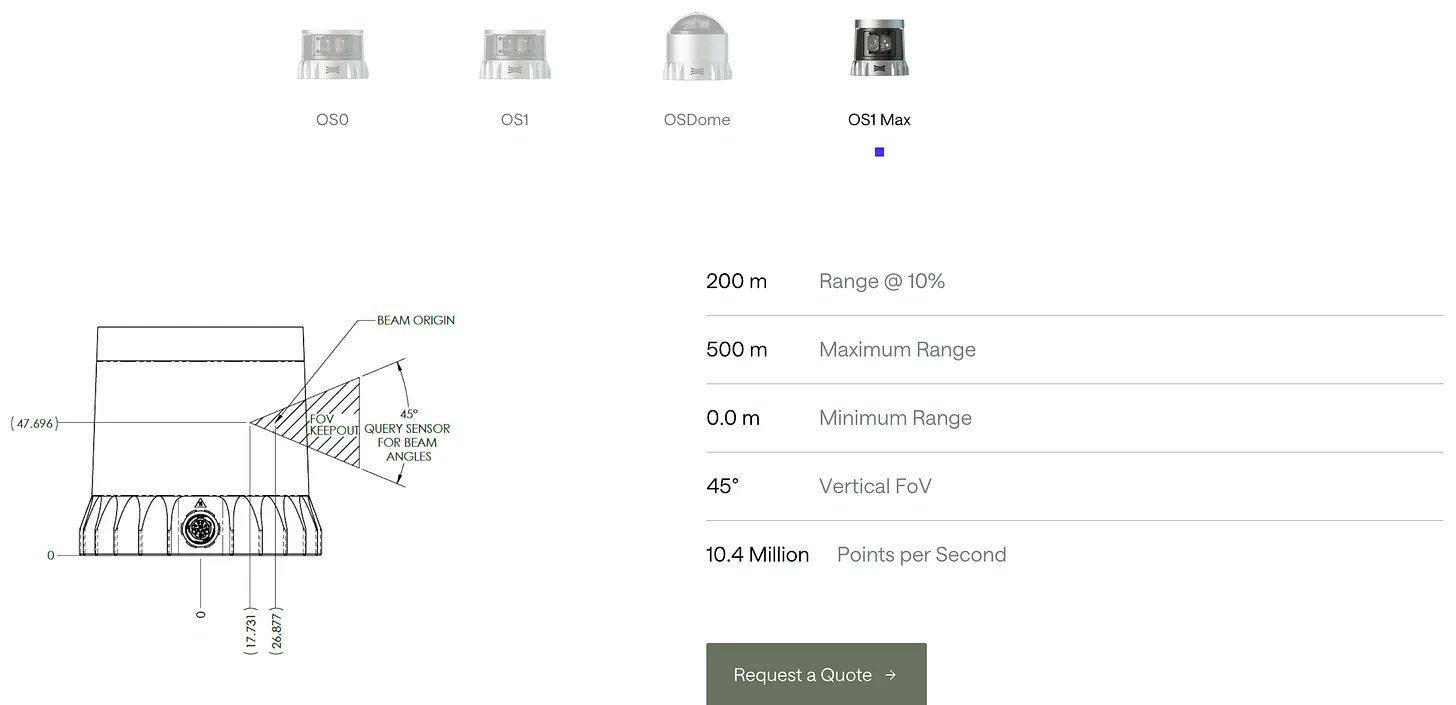

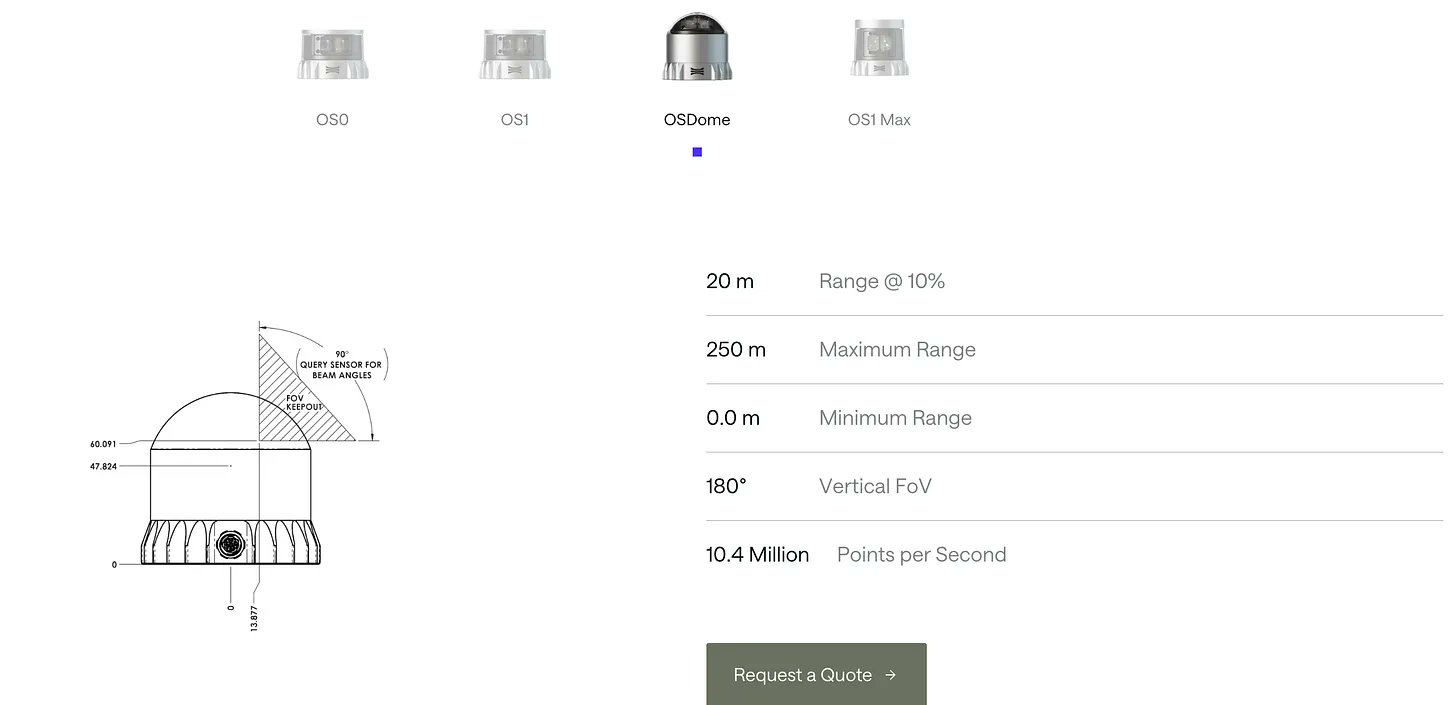

There is a product family here.

- OS0 is more of a short-range / wide-view sensor

- OS1 is the balanced middle product

- OS1 Max is more long range

- O2Dome is a dome-style sensor for wide-area coverage

So the product lineup is basically different ‘eyes’ for different physical jobs.

That’s because these different Physical AI systems have different needs.

For example a mining vehicle does not need the same sensor as a humanoid wrist camera.

Now, Ouster is attempting to make lidar more scalable. The cost of lidar has been a problem in the past. Powerful, but expensive. Their claim is that by using a more semiconductor-like architecture, they can lower cost, improve reliability, shrink the product, and make manufacturing more scalable over time.

Rev8: The New Product Cycle

This is Ouster’s newest lidar platform. And it’s major.

This is no small product cycle refresh.

We’re talking:

- Better range

- Better resolution

- Native color

- Better manufacturability

- More ruggedness

- Deeper relevance to Physical AI

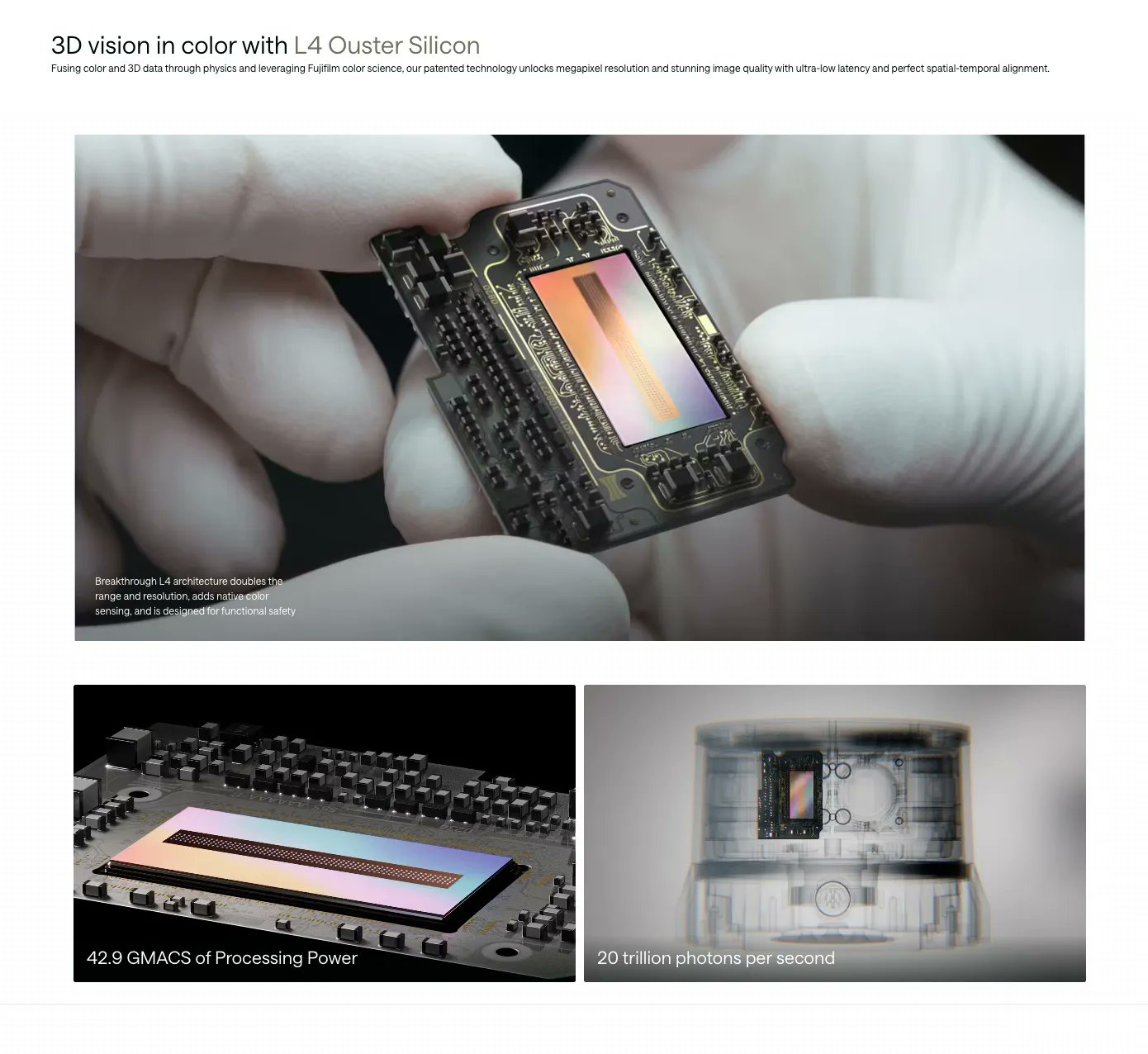

Let’s start with native color lidar.

Remember, traditional lidar gives the 3D structure. Cameras give the machine color and visual context. Typically if a customer wants both, they have to combine these through software. So then they would need to consider calibration, timing, alignment, and integration work.

Rev8 is supposed to make that cleaner by capturing 3D data and color context together.

So why does this even matter? Well, for Physical AI a machine not only needs to know where something is. It needs to understand what it is looking at. Color adds more context here.

Now we also have to talk about L4 Ouster Silicon.

This is the custom chip powering Rev8. They want the chips to keep improving which helps the sensors get better, cheaper, and more scalable over time.

Rev8 is important for a few main reasons:

- It is the current product cycle and what customers are evaluating now

- It strengthens the Physical AI story because native color 3D data can be useful for robots, mapping, smart infrastructure, industrial automation, drones, and training data

- It is where the platform claim has to start proving itself. If Rev8 helps Outser sell more software, integrated perception, robotics workflows, and multi-product systems, then the story becomes much stronger.

Rev8 customer evidence

Product specs are one thing. But we want to know if these are actually pulling customers in.

We’ve got a wide range of logos here across heavy equipment, robotics, drones, mapping, industrial automation, autonomy, and infrastructure-type markets.

This doesn’t mean production revenue. It could mean testing, prototypes, permission etc.

But this does tell us that customers in relevant Physical AI markets are at least engaging with the technology.

Stereolabs

This is where the story moves beyond pure lidar.

Stereolabs gives gives Ouster cameras, robotics vision, depth software, AI compute adjacency, and a developer ecosystem.

So now we have 3D sensing via lidar and visual depth from cameras.

These cameras are better for close-range visual understanding.

A robot arm, humanoid hand, or manipulation system may need what is directly infront of it. This is a much different perception problem.

That brings us to ZED.

ZED cameras are stereo cameras, meaning they use two camera views to estimate depth. Similar to human eyes.

Their latest presentation specifically highlights ZED X NANO.

This is the small camera product they are positioning around robotics and manipulation. This image of it on a robotic arm really makes the use case clear.

Then we have neural depth.

That basically means AI-assisted depth estimation. The camera captures images, and the software helps estimate distance and shape.

This also ties back into Physical AI training data. These robots need real-world examples. TO see objects from different angles, in different lighting, in different positions, with different levels of messiness. A stereo camera can help capture that kind of visual-depth.

So to summarize, stereolabs broadens Ouster beyond Lidar, gives Ouster a cleaner robotics / manipulation angle, and hedges the sensor debate.

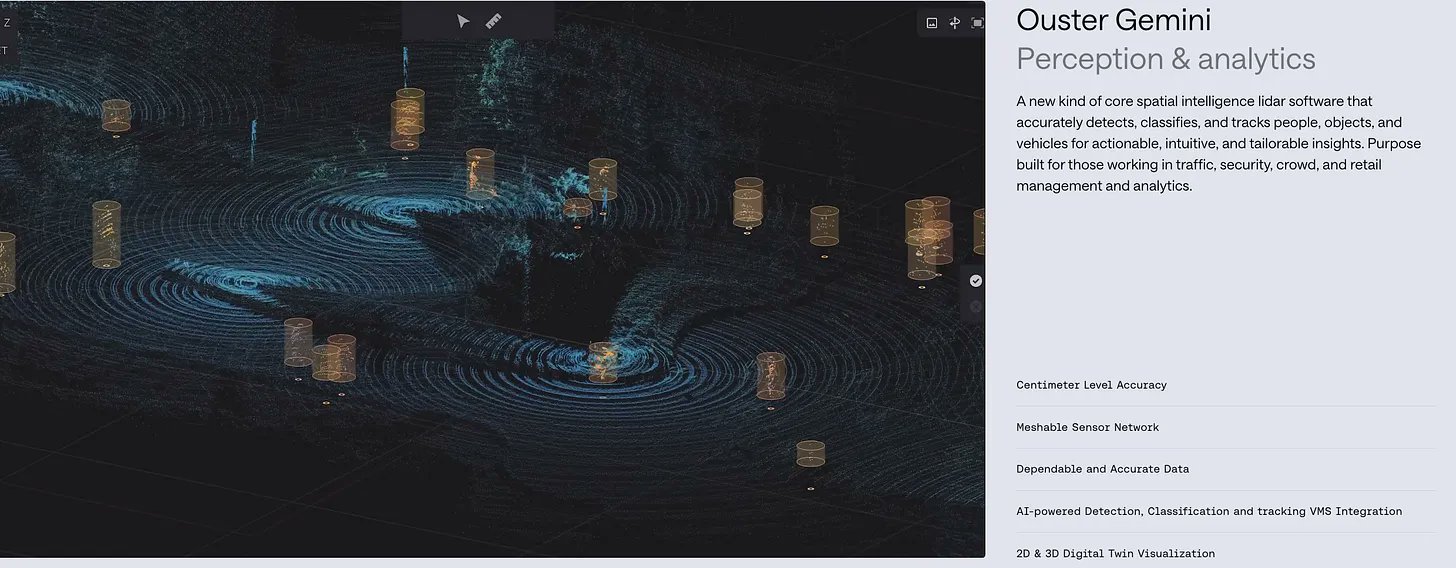

Gemini and BlueCity

This is software / smart-infrastructure section

Up to this point we have talked about the hardware that collects all the information from the phyiscal world.

Now we have to talk about how the customer can actually take all that raw information and use it. Becuase at they end of the day, the customer doesn’t want to just look at a 3D point cloud. They want answers.

Is that a person? Or a vehicle? Is it moving? Is there congestion? etc.

This is where the software comes in.

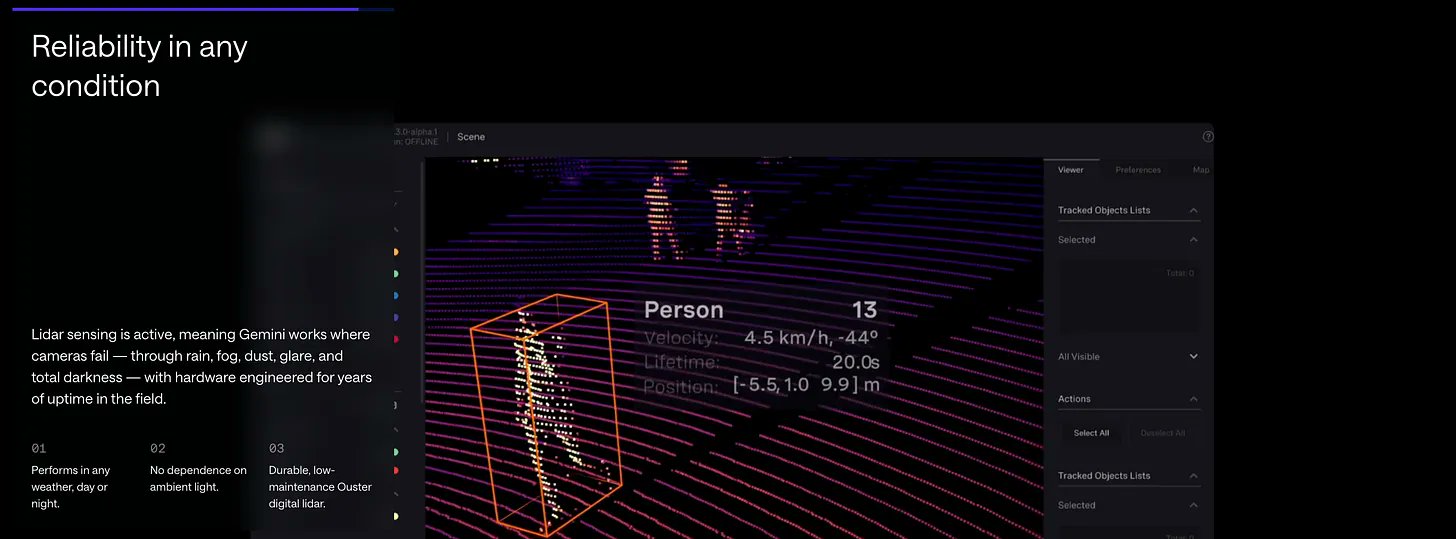

Gemini is the broader perception platform.

Think of it as the layer that takes the sensor data and turns it into object detection, classification, and tracking. In these two pictures you can see the software detecting the humans, how many humans, how long they have been in the frame, their speed, and their location.

BluCity is more specific. It is a traffic-management application built on that perception layer.

This is what cities and transportation agencies can use at intersections, roads, highways, mid-block crossings, and other traffic enviornments.

X Has now limited me from putting any more images in here. So if you would like to continue reading with the images (they are important) click here (no paywall on substack):

https://open.substack.com/pub/cruxcapitalgroup/p/oust-deep-dive-one-of-my-favorite?r=6so16n&utm_campaign=post&utm_medium=web&showWelcomeOnShare=true

Some reasons a city would adopt this is to make intersections safer, move traffic more efficiently, understand dangerous patterns before crashes happen. They could also upgrade infrastructure in a more targeted way.

You could also take that real-time digital traffic and turn it into a digital twin.

📷

So not only are you getting a live feed that you can use to make traffic signals more dynamic (maybe one direction needs a green light for longer) but you can also use this for planning and simulation. We talked a lot about this in previous layers of the Physical AI theme. Once the city has a digital version of the intersection, it can test changes. What happens if they add a bike lane? What about changing the signal timing? Add a protected left turn? The digital twin becomes a way to understand changes to the intersection before literally physically changing it.

What’s also interesting is that this can be more ‘privacy-friendly’.

📷

At first I didn’t really understand why this was that important because I just assumed we are always being filmed when we are walking in major intersections. But this allows a city to track objects and movement in 3D without necessarily needing face-level imagery. They can blur things. If privacy concerns can slow down camera-heavy deployment, this could be the bridge.

End Markets

Throughout this report we have touched upon their end markets, but here I am going to cleanly lay them out. Ouster defines 4 major buckets. And there are some sub-categories within each. I will lay them out as clearly as I can.

📷

Where does a customer actually need 3D perception badly enough to pay for it?

Industrial

This is a very important near term bucket.

Warehouses, ports, factories, yards, mines, construction sites, farms, and heavy equipment. These environments are physical, messy, and safety-sensitive.

A warehouse robot needs to avoid workers and shelves.

📷

A port automation systems needs to track containers, trucks, cranes, and people.

📷

A mining vehicle needs to navigate uneven ground, dust, darkness, and huge equipment.

📷

This is a strong market because customers want spatial awareness and not just images.

Ouster continuously highlights 3 features that are very important for this end market.

1 - Being performant in all lighting conditions.

📷

2 - Being Ruggedized and built for all conditions

📷

3 - Being high resolution

📷

You can see the power that these machines can have and all the use cases for them very clearly.

Industrial also has better economics than other markets in some ways. If a lidar sensor can help prevent downtime, reduce labor pressure, improve safety, or increase throughput, then the customer can justify the capital expense.

This is a real-revenue today market.

Smart Infrastructure

This is the BlueCity / Gemini bucket we just covered.

I feel like I covered those pretty well so I won’t just repeat the same things.

But I want to mention that this expands beyond roads and intersections. Think airports, campuses, stadiums, security zones, retail spaces, public venues in general. These places need to understand what is happening without relying only on humans watching cameras.

Any area where it would be useful to track how many people or objects are there, how long they spend there, analyze trends that you either want to reinforce or reduce the likelihood of them happening again, and so on.

Also the digital twin angle is really important. Making real physical changes can cause a massive headache and be a costly expense if done improperly. Once you have enough data you can simulate changes and see which ones work the best before deploying them.

Deployment Evidence

Now let’s look at some deployment evidence. Ouster says BlueCity has over 700+ contracted intersection and roadway deployments.

Chatanooga expanded BleuCity to 120+ intersections after a 12 month pilot. They use it for traffic flow management and safety incident detection/analytics.

Utah DOT selected BluteCity for 100+ intersections. They evaluated six lidar systems, five met minimum requirements, and the Ouster BlueCity integrated solution received the highest overall vendor score.

Georgie DOT selected BlueCity for 30+ additional intersections around Atlanta, including areas near Mercedez-Benz stadium ahead of the World Cup. Cool use case and you can see the potential hear.

And there are many more wins. The point is that this is happening now and they are having success.

Installation and Maintenance

This is part of the pitch.

Cities don’t want massive road construction everytime they upgrade a censor. Ouster says BlueCity averages 3-5 hours to install, uses existing infrastructure, avoids mast arms/trenching/lane closures, needs no complex calibration, and is low maintenance. The sensors are designed for 250k- hours MTTF (mean time to failure) and a massive temperature range that serves all environments.

This is all important for practical deployment. A traffic department may not choose the most advanced product if it is painful to deploy or expensive to maintain.

Security

Ouster has a whole page dedicated to the security applications here.

📷

I thought this was especially interesting.

📷

‘Small floating objects like a drone or a box being thrown over a fence are now possible to detect’. In this day and age with so much concern about drone capability and threats, I can imagine this will be a use case that will be deployed in all major cities, ports, stadiums etc.

They spend a good amount of time talking about false alarms and situational awareness.

📷

They say that lidar + Gemini can create a PIDS (perimeter intrusion detection system) and estimates it can reduce nuisance alarm rates by 95%.

Security teams do not want a stream of noise alerts. They only want true alerts. If a system is constantly getting triggered, operators stop trusting it.

📷

Anyone get the reference? Alright, that’s my one joke for the day.

Ouster is pitching Gemini as a way to trigger alarms more accurately. That’s the idea.

Crowd Analytics

Airports, hospitality, retail, transit hubs, stadiums, music venues.

Queue management, dwell-time measurement, user-journey tracking, staffing optimization, privacy-preserving analytics.

This is where the digital twin idea can come in place again. If you want to maximize efficiency in an airport to reduce lines and waiting time, you have enough data to manipulate different factors digitally and see how it plays out. Before taking the risk of implementing it in real life.

Robotics / Drones

Now we’re talking! The cool stuff.

This is the most ‘thematic’ bucket people would probably think of with Physical AI. But remember, it’s not just humanoids.

We’re talking mapping, inspection, SLAM (we’ll get to this in a second) autonomous mobile robots, defense ground vehicles, surveying drones, confined-space drones, agriculture/forestry drones, and now Stereolabs-style camera-based robotics vision.

SLAM. Simultaneous localization and mapping.

That just means the robot is doing two things at once. It is building or updating a map of the environment and it is figuring out where it is inside that map.

📷

Ouster’s own SLAM explainer says SLAM helps robots estimate their position and orientation while creating a map, which is what allows autonomous robots to navigate. It gives examples like vacuums, last-mile delivery robots, warehouse robots, mineshafts, volcanic tunnels, and other unknown environments. Ouster also says lidar-based SLAM uses distances and shapes from the sensor, and is better suited to creating a realistic 3D digital twin copy of a map than camera-only approaches.

That is the practical reason robotics customers use lidar.

Mapping, surveying, and inspection

The customer wants a 3D map or a 3D inspection model. Lidar directly creates 3D data.

📷

Higher-resolution sensors can help handheld mapping collect effective data from fewer passes, drone inspection benefits from lighter lidar and longer range, and agricultural/industrial inspection needs enough detail to map and inspect high-value assets with centimeter-level precision.

If you are inspecting a bridge, mine, tunnel, cargo ship, sewer, utility asset, or industrial site, you may not need a humanoid robot. You may just need a drone or mobile robot with a strong 3D sensor.

Send fewer humans into dangerous places.

Inspect faster.

Create a precise 3D model.

Reduce downtime.

Lower inspection cost.

Robot deployment and SLAM maps

A lot of autonomous robots need a high-quality map before they can operate well. That map may be created by a robot, a handheld system, a backpack, or a drone.

📷

The dConstruct case study explains this well. dConstruct uses Ouster digital lidar in a lightweight mapping backpack called dASHPack. The system includes an OS1-32 lidar, an IMU (Inertial Measurement Unit), and four RGB (color) cameras. It creates HD point-cloud maps over 500 square meters in 20 minutes or less, and Ouster says the combined dASHPack / dASHXplorer workflow can produce a detailed map in about 30 minutes. Those maps can then help deploy autonomous robots such as cleaning robots, last-mile delivery robots, and inspection robots.

📷

Defense Ground Robotics

Keep soldiers out of dangerous vehicles or dangerous routes. Simple.

📷

Forterra is the key Ouster case study. Forterra develops ground-based vehicle autonomy for defense. Ouster says Forterra’s AutoDrive platform uses multiple Ouster OS digital lidar sensors, plus cameras and radar, for maximum visibility around the vehicle. The environments are exactly where perception gets hard: off-road, GPS-degraded, low-light, foggy, dusty, rainy, unfamiliar terrain, no lane markings.

Ouster says Forterra was selected for four active DoD programs and has shipped over 100 vehicles, operated 400,000 cumulative miles, and has technology operating in U.S. military programs in more than ten countries.

Here is a great example of lidar in a non-consumer car vehicle context.

Drones for agriculture, forestry, and snow operations

Ok last one. I need to move on. But there are so many cool use cases.

This part is a bit niche, but it shows breadth.

📷

Deep Forestry built a push-button autonomous survey drone for dense, cluttered environments such as industrial buildings, warehouses, underground tunnels, and agricultural/forest management. The point is that forest and agriculture environments are messy, dense, and hard to map manually.

Microavia is another niche example.

📷

Ouster says Microavia uses pre-programmed autonomous missions and self-charging drones to monitor snow distribution at ski resorts, extend opening seasons, and support avalanche control, detection, and mitigation.

These are not huge standalone buckets today, but they show why the drone market is so much more than consumer + defense.

There is also the Rev8 deployment on robotic arms but we covered that earlier.

Automotive

This gets far more attention than it probably deserves.

Let’s break this into a few buckets.

- Consumer ADAS (Advanced Driver Assistance Systems). Gosh I really don’t like this one personally. But I guess I would appreciate it being there if we I ever did need it. Adaptive cruise control, lane keeping, automatic breaking etc. Their argument is that lidar direct 3D measurement can improve long-range object detection, small-object detection, and overall perception.

📷

- Robotaxis.

Much higher autonomy requirements than consumer ADAS.

“Fleet operators are able to offer more rides at an affordable price point by decreasing vehicle downtime and removing barriers to access for underserved neighborhoods and populations. The advent of push button ride service has already had a significant impact on instances of drunk, tired, and dangerous driving. This will take it a step further.”

📷

- Autonomous Trucking

Long haul, yard trucks, mining trucks, construction vehicles.

“One in every three truck drivers will be involved in a serious accident at some point in their career”. Wow, I would not have guessed it was that high.

📷

- Shuttles and buses.

Defined routes. Makes autonomy easier than completely open-world passenger driving.

📷

Manufacturing, Supply Chain, and IP

Can Ouster scale and defend it’s business?

First is manufacturing scale. Their 10-k says that they designed their digital lidar tech for high-volume manufacturing and that Benchmark and Fabrinet (hey, we know you!) manufacture the majority of it’s products. This should help reduce product costs and let it scale production as demand grows. That is great. It doesn’t need to own every factory. Leverage your large manufacturing partners to scale faster.

They also pitch this as a ‘scalable global fulfillment model’.

📷

So they offer scalable outsourced manufacturing and local fulfillment in three major global regions, with the goal of faster lead times and lower total costs.

Then there is the reliability aspect that we spoke about earlier.

📷

These machines are not being used in clean, calm environments. So the idea that these can be used in real, harsh environments pushes it as a real and ready product.

Now the Government / infrastructure procurement angle.

This is where Ouster might have a real advantage in certain markets.

📷

Ouster says its Buy American and Buy America certified sensors qualify for purchases by government agencies using federal funding and grants. The same article says those certified sensors are considered 100% manufactured in the United States and 100% made from U.S. domestically sourced materials. That does not apply to every Ouster sensor globally, but it matters for federally funded infrastructure, transit, security, and public-sector deployments.

Defense is similar. Ouster says its OS1 sensor was approved by the Department of Defense for unmanned aerial systems and added to the Blue UAS Framework.

📷

They frame that as NDAA compliance, supply-chain security vetting, and streamlined procurement for U.S. government agencies and partners. It also says Ouster technology is deployed in systems used by the U.S. Army, U.S. Navy, National Laboratories, NASA, and Department of Transportation-funded projects.

That matters because cheap Chinese lidar may win some commercial markets on price. But in government, defense, critical infrastructure, and federally funded transportation, customers may care about trusted supply chain, compliance, cybersecurity, and domestic manufacturing options.

The last piece is IP and defensibility. Ouster says its IP covers digital and analog products and solutions, including software, real-time 3D vision for autonomous systems, manufacturing processes, and calibration methodology. It also says it owns patents, designs, copyrights, trademarks, trade secrets, and other rights, while noting that no single patent or IP right alone protects the whole business.

That last bit is important. I don’t think the moat is one specific patent. It’s more likely the combination of all the different bits put together. Like the custom chips, digital lidar architecture, rugged product deisgn, software etc.

Finances

The first thing to understand is that Ouster is already a real revenue business. In Q1 2026, they reported about $49 million of revenue, up 49% year over year, with 12,600+ sensors shipped. That included 8,300+ lidar sensors and 4,300+ camera sensors.

📷

Let’s unpack a bit.

- Product revenue is important. Royalty revenue was not material in Q1 and management said total 2026 royalty revenue should be less than $5m and most in the back half. So Ouster is still a cleaner product business.

- Lidar-only business grew about 44% YoY. So the legacy core is not being masked by Stereolabs. Lidar is still growing strongly on it’s own.

- Stereolabs is already contributing though. They had about 7 weeks of Streolabs contribution in Q1 and still shipped 4,300 camera sensors.

- Smart infra & industrial are the current anchors. #1 and #2 in revenue contribution Q1.

- BlueCity has 700+ contracted site deployments across intersections, mid-blocks, and highways. Gemini had a significant customer renewal, produced millions of revenue, is deployed at 550+ sites, and uses a model trained on 4M+ labeled objects. These are the best evidence that Ouster is trying to move beyond raw sensors into software-enabled perception systems. But we still need more disclosure on how much of that is recurring software versus hardware/project revenue.

- Rev8 is also a scale/cost story. Rev8 was designed to be more affordable and more scalable than Rev7. Management said OS1 Max may command premium ASPs in some domains, but the broader Rev8 upgrade should not disrupt customer economics. So, better capability, broader adoption, more scalability, and maybe premium pricing in specific high-end use cases.

- Profitability path is plausible, but not done. Q1 GAAP gross margin was 43%. Adjusted EBITDA loss was . Cash / restricted cash / short-term investments were $175M, with no debt. Q2 revenue guidance is $49.5M–$52.5M. Management’s long-term framework is 30%–50% revenue growth, 35%–40% GAAP gross margin, and 5%–8% OpEx growth from 2025 levels.

Competition / Defensibility

Can anyone else copy this, undercut them, or make the product less valuable?

Ouster’s own 10-K is pretty direct about the risks. They say revenue and margins could be hurt if they cannot maintain competitive ASPs, high volumes, or lower product costs. So Ouster is telling us the hardware business has pricing pressure risk. They also explicitly say they compete with established companies that have more resources, new entrants, and alternative technologies, and that lidar adoption itself is still uncertain.

- Hesai is probably the most important direct lidar competitor to mention. Hesai has a very broad lidar portfolio across ADAS, robotaxis, robotrucking, robotics, warehousing/logistics, stationary applications, and spatial sensing. Its product page shows long-range automotive lidar, short-range solid-state lidar, mini 360° lidar, mid-range lidar, and high-performance 360° lidar. That overlaps a lot of Ouster’s potential markets.So I see Hesai as the price and scale threat. If lidar becomes a commodity hardware market, Chinese suppliers like Hesai can pressure margins. But Ouster’s defense is Western supply chain, compliance, software, BlueCity/Gemini, Rev8 native color, and industrial/infrastructure relationships.

- RoboSense is also very relevant. Its site lists LiDAR for Automotive, LiDAR for Robotics, and also Active Camera products for robotic movement and hand-eye coordination. That makes it interesting because it partially mirrors what Ouster is trying to do after Stereolabs: lidar plus robotics vision. So RoboSense is not only a price competitor. It is a strategy competitor. Ouster is saying, “We are becoming lidar + cameras + perception software for Physical AI.” RoboSense is also pushing into lidar plus robot sensing.

- Aeva’s pitch is different from Ouster’s. Ouster’s Rev8 is native-color 3D lidar. Aeva’s pitch is 4D FMCW lidar, which means it measures 3D position plus velocity. Aeva’s sensors as give equipment and vehicles a 3D view while also detecting how fast surrounding objects are moving.This matters most in high-speed autonomy, trucking, robotaxis, and dynamic environments. Aeva is not the main competitive threat to Ouster’s smart infrastructure or industrial business today. But it is relevant because if the market decides velocity-per-point is critical, Aeva has a differentiated architecture. Ouster = 3D + native color + rugged scalable digital lidar + software. Aeva = 3D + velocity / 4D motion sensing. Aeva is another company that I am interested in investing in for my Physical AI basket.

And so on. There are more competitors.

It is really four battles.

First is lidar versus lidar. Ouster has to compete against other lidar companies on range, resolution, reliability, cost, size, power, functional safety, and manufacturability.

Second is lidar versus other sensing architectures. Some customers may choose cameras, stereo cameras, radar, or a cheaper mixed stack instead of lidar.

Third is hardware versus software value capture. If Ouster only sells sensors, customers or integrators may capture more of the software and application value. Gemini and BlueCity are Ouster’s attempt to move up the stack.

Fourth is China / cost pressure. Chinese lidar suppliers can be aggressive on cost. Ouster’s defense is not just “better specs.” It has to be digital architecture, custom silicon, reliability, compliance, software, customer relationships, and Western supply-chain trust.

The strongest thing Ouster has going for it is that it is not concentrated in one market. We spend lots of time going over all their markets + use cases. So Ouster is not fully dependent on one passenger car cycle or robotaxi program.

The second advantage is the digital lidar architecture. Their 10-K says the digital products use VCSELs, SPADs, in-silicon signal processing, custom system-on-chip technology, and patents around lidar-camera convergence. Like I mentioned, Ouster is trying to make lidar more like a semiconductor product: more integrated, more scalable, and less dependent on lots of discrete analog parts.

Another advantage is Rev8. This is the product that can help them defend the core. The first Native color lidar, L4 silicon, OS1 Max, 256 channels, long range, high point density, and functional-safety design all give Ouster a stronger product story.

Then we have breadth after Stereolabs. Ouster is less vulnerable as a lidar-only company now because Stereolabs gives them stereo cameras, neural depth, robotics vision, and AI compute adjacency. If a robot uses cameras instead of lidar for manipulation, Ouster can still have a product in that architecture.

And lastly, software / application layer. Gemini and BlueCity are the clearest proof here. A raw lidar sensor can be swapped more easily than an installed traffic-management system or perception workflow. If Ouster becomes embedded in intersections, security systems, crowd analytics, ports, warehouses, and robotics workflows, replacement becomes harder.

Valuation Framework

At roughly $42 per share, the company is worth about $2.7 billion in market cap. Its 52-week high is $51.50.

The question is whether the company can grow into a premium valuation and then keep expanding it as the market starts treating Ouster less like a lidar hardware supplier and more like a Physical AI perception platform.

For 2026, I think a reasonable base case is roughly $220 million to $235 million of revenue. That assumes Q1 and Q2 are not one-offs, Stereolabs contributes for the full year, smart infrastructure remains strong, industrial keeps growing, and Rev8 starts contributing more meaningfully in the back half.

For 2027, I would use roughly $340 million to $380 million of revenue. That assumes Rev8 adoption builds, BlueCity continues to scale, Stereolabs becomes more integrated, and Ouster keeps compounding well above a normal hardware growth rate.

For 2028, a base case of $500 million or more is not unreasonable if the Physical AI cycle keeps broadening and Ouster continues to execute. That is where the model starts to get much more interesting, because revenue scale plus stable gross margin can create real operating leverage.

The path to profitability is also becoming visible.

The CFO’s framework is 30% to 50% revenue growth, 35% to 40% GAAP gross margin, and controlled operating expense growth. If Ouster gets to $340 million to $380 million of revenue while holding gross margins around 40%, adjusted EBITDA profitability becomes much more realistic.

That is why 2027 matters so much. The market is already looking through today’s losses and paying for that path.

The bear case is still very real. If Rev8 adoption is slower than expected, if camera mix pressures average selling prices, if software revenue stays hard to see, if Chinese lidar suppliers pressure pricing, or if the market decides Ouster is still mostly a hardware company, the multiple can compress quickly.

In that case, I would use a 12-month bear range of $30 to $38.

That is not a disaster scenario. That is more of a “the company is fine, but the multiple cools off” scenario.

My 12-month base case is higher: $60 to $75.

That assumes Ouster keeps beating the old lidar-company perception, Rev8 adoption becomes more visible, Stereolabs keeps adding to the robotics story, BlueCity wins remain strong, and the market continues to reward OUST as one of the cleaner public Physical AI perception plays.

My 12-month bull case is $90 to $100.

That would require a strong Rev8 ramp, more named production adoption, clearer evidence of software attach, continued smart infrastructure wins, and a market that becomes more comfortable giving Ouster a premium platform multiple.

For the 24-month framework, I would use:

Bear case: $35 to $40.

Base case: $100 to $120.

Bull case: $140 to $160.

The 24-month base case assumes Ouster is approaching or passing $500 million of revenue, adjusted EBITDA has turned positive or is clearly there, and the market is no longer debating whether this is just a lidar company. In that version, Ouster becomes one of the few liquid public ways to own Physical AI perception across lidar, cameras, smart infrastructure, robotics, industrial automation, and software.

The 24-month bull case assumes something more powerful. Ouster proves that Rev8 is not just a better sensor, but the start of a larger platform cycle. That would mean customers are buying more of the stack. Lidar, cameras, AI compute, Gemini, BlueCity, and software begin showing up as a more integrated business.

That is where the multiple can stay elevated.

Now they have to continue to earn it.

The four things I am watching most closely are revenue growth, gross margin quality, software attach, and progress toward profitability.

If those improve together, I think the base case is meaningfully higher than where the stock trades today.

If revenue grows but the business still looks mostly like hardware, the stock can still work, but the upside is much more limited.

That is the valuation setup.

Please keep in mind that these are my own personal financial modeling scenarios and are not formal price targets.

If you enjoyed this article, please consider subscribing to my substack! On there I am building out my entire Physical AI portfolio & research. I will be diving just as deep into all of the relevant companies. I will also be 'covering' these companies closely. So that includes earnings calls, presentations, trying to get in touch with executives, stress testing the thesis etc.

You can click the link in my bio to sub!

If not, no worries. Please consider sharing this post at least!

Financial Disclosure and Disclaimer

At the time of publication, I do not own shares of Ouster. I am actively researching the company and may initiate a position at any time, including shortly after publication, depending on valuation, price action, portfolio construction, new information, risk management, or changes in my thesis.

This report is for educational and informational purposes only. It reflects my personal research process, opinions, and interpretation of publicly available information. It should be treated as general market commentary, not individualized investment advice, financial advice, legal advice, tax advice, or a recommendation to buy, sell, hold, short, or avoid any security.

Nothing in this report should be relied upon as a complete analysis of Ouster or any other company mentioned. The companies discussed may carry significant risk, including valuation risk, dilution risk, customer concentration, product delays, competitive pressure, margin pressure, supply-chain risk, tariff risk, execution risk, acquisition integration risk, technology risk, regulatory risk, and stock-price volatility.

I may buy, sell, add to, reduce, avoid, or change my view on any company mentioned at any time without prior notice. My personal investment decisions may differ from the opinions expressed in this report, and my views may change as new information becomes available.

Any financial figures, product claims, customer relationships, management commentary, market forecasts, valuation ranges, or scenario frameworks discussed in this report are based on publicly available information believed to be reliable at the time of writing. However, company statements, projections, market expectations, and my own assumptions may prove inaccurate or incomplete. Future results may differ materially from current expectations.

Readers are responsible for their own due diligence. Please review company filings, earnings calls, investor presentations, balance sheets, competitive positioning, valuation, risks, and your own financial situation before making any investment decision. Consider consulting a qualified financial adviser, tax professional, or legal adviser if needed.